Behavioural research

Why Do Investors Fire Their Financial Adviser?

Our findings suggest a few common issues; however, they are multifaceted. Many of these issues can be traced back to three underlying drivers that advisers should pay heed to and can remedy.

Introduction

What motivates an investor to fire their financial adviser? Obviously being fired is not a good thing for a financial adviser, as it results in lost business from the client but also lost referrals and potential clients being discouraged by negative reviews. Naturally, any adviser would be interested to know how to prevent such setbacks in their practice. Moreover, answering this question also gives broader insight into potential issues in an adviser-client relationship. Even when these issues are not problematic to the point of termination, they can still undermine business in the form of behavioural issues, lack of engagement, or ungiven referrals.

In this research, we endeavored to better understand the motivations behind firing decisions. Our findings suggest a few common issues; however, they are multifaceted. Many of these issues can be traced back to three underlying drivers that advisers should pay heed to and can remedy: 1) insufficient focus on the person side of personal finance; 2) advisers’ inability to communicate their value; and 3) a mismatch of expectations early in the relationship.

Financial Reasons Just Scratch the Surface

It’s easy to blame firing decisions on conspicuous reasons, such as lackluster returns or high costs, but previous research examining why investors fire their financial advisers has found a much more complex story. Recent research by The Ensemble Practice1 found that, along with cost and performance reasons, many investors identified lack of communication and listening skills as the drivers of their firing decision. However, the largest portion of respondents selected “other” to explain their decision, meaning thatpeople’s firing reasons may be complicated and difficult to categorise. Other research2 examined why individuals fired their advisers during the Great Recession and found that “loss of net worth” was not a primary driver; in fact, variables related to money in general (for example, reported decrease in income) were not the main reasons given for why advisers were fired. Given previous findings, it is clear that the reasons are complicated, and simple accounts that focus exclusively on return performance may miss the mark

“Why Did you Choose to Stop Working With an Adviser?”

To better understand what motivated investors to fire their advisers, we asked those who had terminated services with an adviser the following question: “Why did you choose to stop working with [an] adviser?” The question was open-ended, allowing us to collect people’s thoughts in their own words. We featured this question in three different surveys, which included a total of 3,003 people, conducted during specific periods of 2021 and 2022.3 Using this strategy, we were able to collect 184 total responses from people who indicated that they had terminated services with an adviser.

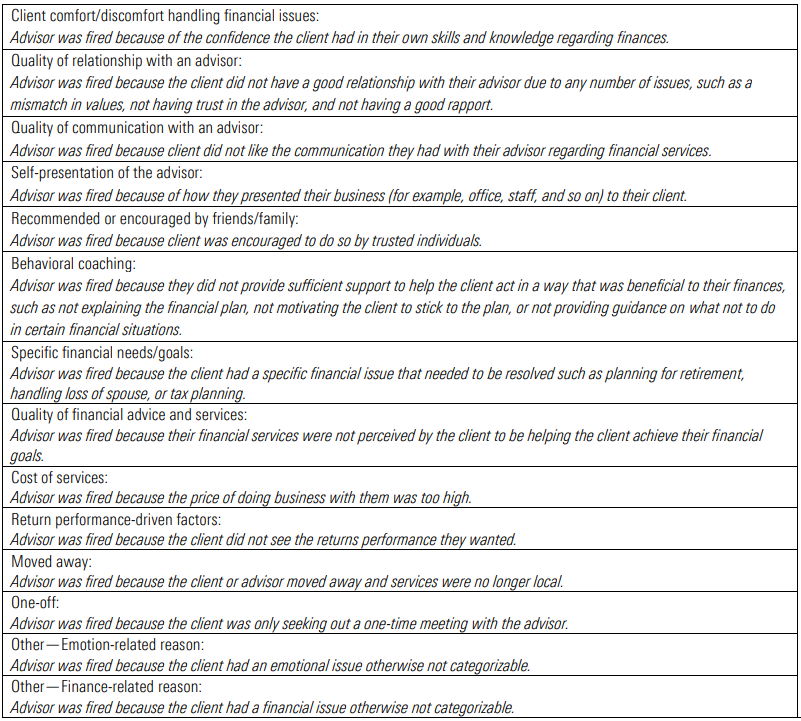

To analyze the data, we began by looking to existing research4 to identify common motivations behind an investor’s decision to fire an adviser (Exhibit 1). Using this master list of common motivations, we manually categorised each response into one or more motivation categories.5 Using this technique, each response could be assigned to multiple motivations, based on how many topics a person brought up in their explanation of their reasons.

Exhibit 1: Common Motivations Behind Firing Decisions

Source: Morningstar Research

Who Fires Their Adviser?

We began our analysis by asking “Who has ever fired their adviser?” Out of the 3,003 people who received one of the three surveys, only 185 individuals marked that they had fired an adviser in the past. In other words, only 6% of our sample ever felt the need to break a relationship with an adviser, which generally means that firing is a relatively rare occurrence and is good news for advisers. However, existing research6 notes that many people stick with their adviser because they don’t want to incur the cost of switching; instead, they choose to move assets out of an advisers’ practice instead of ending the relationship entirely. We did not address this kind of disengagement and instead focused on cases where there was a clear break.

To identify whether certain individuals were more likely to fire their adviser, we compared individuals who had and had not fired an adviser by certain demographics. We started by subsetting the data to include only individuals who currently have an adviser (N = 484), allowing us to ensure that our sample is relevant to advisers’ typical client base. Our results suggest that individuals who have a higher income,7 higher amount of investable assets,8 and a higher level of financial literacy9 are more likely to have fired an adviser in the past. We also found that those who are older10 are more likely to have fired an adviser in the past—however, we recognise that this may be a spurious effect and the result of having had more experience working with financial advisers. When looking at gender, we did not find that either gender11 was more likely to have fired an adviser.

ADVERTISEMENT

Morningstar’s trusted independent fund manager research thinking employed in an implemented portfolio. Request a call back now.

Making Sense of Open-Ended Responses

To examine participants’ open-ended responses, we first had to read through each participant’s response and identify which of the categories in Exhibit 1 they fell under. Note that responses could fall under multiple categories because participants could give several reasons within their responses. For example, one participant responded, “No input. Mediocre advice. High fees.” Their brief answer indicates that they had several reasons for firing their adviser, including Quality of Communication with Adviser (“No input.”); Quality of Financial Services and Advice (“Mediocre advice.”); and Cost of Services (“High fees.”). Some of the responses we saw in the dataset were equally laconic, whereas others were quite verbose.

Organising Open-Text Responses Into Categories

Given that human raters categorised participants’ responses, we first established inter-rater reliability between the two raters to make sure they were aligned with each other in their approach. Inter-rater reliability measures the degree to which the two raters agree with each other on the categorisation; this is done to ensure that responses are categorised in a consistent manner across individuals and there is good quality in the measurement process.12 This validation allows raters to establish a standard way of approaching responses. To illustrate, consider the responses “he insulted me lol.” Though this answer is about a communicative act (insulting), raters established that Quality of Communication with Adviser needed to reflect issues regarding the communication between advisers and clients relevant to the financial advising process. As such, this response was also coded as Quality of Relationship with Adviser since the exchange of insults indicates a negative aspect of the relationship.

Once we achieved sufficient reliability, we proceeded to categorise all the responses into the different categories. See Exhibit 2 for an example of how various responses would be classified into six common categories.

Exhibit 2: Categorisation of Responses Examples

Source: Morningstar Research

What Categories Are the Most Influential?

Once we categorised the responses, our next step was to identify the frequency of each of the different reasons. In other words, what causes do investors cite most often when explaining why they fired their adviser? We found the two most cited reasons investors fired their adviser were the Quality of Financial Advice and Services (32% of responses) and the Quality of The Relationship (21% of responses) categories. Responders also tended to cite Cost of Services (17%), Return Performance (11%), as well as their Comfort Handling Financial Issues on Their Own (10%) as reasons for firing (see Exhibit 3 for the six most common reasons for firing an adviser).

Overall, we found that clients fired their advisers for several reasons, not only because of cost and return performance, but also because of things like the relationship and communication they had with their financial adviser. The quality of financial advice and services was most frequently cited as the reason for firing a financial adviser, but the quality of relationship and cost also appeared more often than many of the other categories.13 This suggests that although there are recurring themes for why advisers are fired, assumptions as to why investors fire their adviser may be overly focused on returns.

Exhibit 3: Six Most Common Reasons for Firing an Adviser

Source: Morningstar Research

Takeaways for Advisers

Once we identified why individuals fire financial advisers, naturally, our next question was: “What can advisers do to reduce the chances of being fired by their clients?” To answer this question, we gathered insights from existing literature to identify ways for advisers to address the six most commonly cited reasons we found for firing an adviser.

Exhibit 4 connects each of these reasons to three overarching lessons for advisers along with practical ways advisers can implement these insights. For example, if a person is unsatisfied with their financial adviser for reasons pertaining to Quality of Relationship or Quality of Advice, an adviser can work on emphasising the person side of personal finance. In our data, when an investor citied a reason related to these categories, the issue often stemmed from an adviser not dedicating enough time to understanding who their client is as a person and what their personal financial needs/goals are. Even some reasons related to a specific issue with an adviser’s services seem to start with an adviser not recognising the client’s need for a particular service. Many of these issues could be remedied by devoting more time, attention, and resources to understanding the client, and perhaps leveraging help from established discussion guides, checklists, and exercises.

Similarly, we found a specific underlying motivation for the categories of Communication, Comfort Handling Financial Issues on their Own, and Cost. Each of these categories reflects a need to effectively communicate the value of a financial adviser. Though there will be some cases where a client no longer needs a financial adviser, there is often just a misunderstanding of the value advisers bring to the table. Many individuals who cited Communication as their firing reason indicated that since they haven’t heard from their adviser, the adviser must not be doing anything. Although an adviser may be diligently monitoring their clients’ accounts, if that work is not communicated, it may go unrecognised by clients. Lastly, the firing reason of Cost is more nuanced than at first glance. Of course, there will be instances where a service is too expensive for an individual, but other times, the individual may not believe the value of the service justifies the cost. In general, these issues can be addressed by effectively communicating value using tactics like reaching out to clients proactively, being available through different channels, and keeping clients updated on what market movements mean for them.

Reasons related to Return Performance Driven Factors often seem to stem from a persistent misconception in finance. Unfortunately, some investors seem to continue to associate advisers with generating outsise returns and are quick to point a finger when markets go awry. These issues can be prevented by setting expectations early in the relationship by emphasising the importance of perspective and by helping clients focus on their long-term goals and not short-term returns.

Exhibit 4: How To Not Get Fired

Source: Labotka & Lamas (2023). Why do investors fire their adviser? Morningstar Wealth

The Complexity of Firing Decisions

Asking why investors fired their financial adviser provides us with a better understanding of the various things that can go wrong in an adviser-client relationship. In our study, we do find that instances of firing are relatively rare, but nonetheless terminations do happen and the consequences are damaging to an adviser’s practice. Our findings suggest that investors are most commonly motivated by reasons pertaining to Quality of Relationship and Quality of Financial Advice when firing a financial adviser. However, identifying surface-level reasons for firing is just the first step toward a solution. To understand how to ameliorate these issues, advisers should focus on the underlying drivers, three of which we identified in this research: 1) insufficient focus on the person side of personal finance; 2) advisers’ inability to communicate their value; and 3) a mismatch of expectations early in the relationship.

This article was written by Danielle Labotka, Behavioural Scientist and Samantha Lamas, Senior Behavioural Researcher.

1

Palaveev, Philip. (n.d.). “Why People Fire Advisers.” Retrieved July 8, 2022, from https://www.fa-mag.com/news/why-people-find-advisers64599.html

2

Cheng, Y., Kalenkoski, C. M., & Gibson, P. (2019). “Factors Associated With Hiring and Firing Financial Advisers During the Great Recession.” Journal of Financial Counseling and Planning, 30(2), 289-303.

3

Participants were first asked if they had ever chosen to stop working with an adviser. If they responded yes to this question, they were then directed to the open-ended question. In two of the surveys, participants were shown this initial question if they had investable assets. In one survey, participants were shown this question if they noted that they received financial advice in a previous question.

4

Costa, P., & Henshaw, J. E. (2022). “Quantifying the investor’s view on the value of human and robo-advice.” Vanguard; Marco, M., Pelligra, V., Martignon, L., & Berg, N. (2014). “Retail investors and financial advisers: New evidence on trust and advice taking heuristics.” Journal of Business Research, 67, 1749-57; Cummings, Benjamin F. and James, Russell N., “Determinants of Seeking Financial Advice Among Older Adults” (March 2, 2014). Available at SSRN: https://ssrn.com/abstract=2434268.; Kimiyaghalam, F., Mansori, S., & Safari, M. (2016). “Who Seeks A Financial Planner? A Review of Literature.” Journal for Studies in Management and Planning, 02, 170-89.; Luther, R., Coleman, L. J., Kelkar, M., & Foudray, G. (2018). “Generational differences in perceptions of financial planners.” Journal of Financial Services Marketing, 23(2), 112-127; Stolper, O., & Walter, A. (2019). “Birds of a Feather: The Impact of Homophily on the Propensity to Follow Financial Advice.” The Review of Financial Studies, 32(2), 524-63.

5

To ensure the quality of the manual coding, we first established inter-rater reliability—as established by a Krippendorff’s alpha ≥ 0.64—on 20% of the data.

6

Cummings, Benjamin F. and James, Russell N. “Determinants of Seeking Financial Advice Among Older Adults.” (March 2, 2014). Available at SSRN: https://ssrn.com/abstract=2434268.

7

The difference in the average income between those who have not (M = 121,530, SD = 115,160) and have fired (M = 178,500, SD = 347,587) their adviser (t(483) = 2.57, p < 0.05, d=0.22) was statistically significant.

8

The difference in the average investable assets between those who have not (M = 543,524, SD = 975,965) and have fired (M = 1,022,836, SD = 1,501,407) their adviser (t(483) = 3.37, p < 0.05, d=0.38) was statistically significant.

9

The difference in the average financial literacy level between those who have not (M = 2.76, SD = 0.56) and have fired (M = 2.96, SD = 0.20) their adviser (t(483) = 2.44, p < 0.05, d=0.47) was statistically significant.

10 The difference in the average age between those who have not (M = 48.92, SD = 14.08) and have fired (M = 55.64, SD = 13.00) their adviser (t(483) = 3.59, p < 0.05, d=0.50) was statistically significant.

11 The difference between the proportion of participants by gender who have and have not fired an adviser (X2 (1, N = 483) = 0.001, p > 0.05) was not significant.

12 To establish reliability, raters both categorised the same subsample of 20% of the total responses. Raters were found to agree with each other on average 98% of times across all the categories and reliability was established (mean Krippendorff’s α = .80). Disagreements were discussed and resolved by the two raters.

13 The difference between the proportion of responses in the Quality of Financial Advice and Services category versus others (Cochran’s Q (4, N = 184) = 36.22, p < 0.05) was significant. The difference between the proportion of responses in the Quality of Financial Advice and Services category versus Quality of Relationship with Adviser (Cochran’s Q (1, N = 184) = 6.37, p < 0.05), Returns Performance (Cochran’s Q (1, N = 184) = 20.63, p < 0.05), and Comfort Handling Financial Issues (Cochran’s Q (1, N = 184) = 23.03, p < 0.05) was significant. The difference between the proportion of responses in the Cost of Services category versus Comfort Handling Financial Issues (Cochran’s Q (1, N = 184) = 4.67, p < 0.05) was significant.